Тема: ANALYSIS OF THE RELATION BETWEEN PRIVATE EQUITY INVESTMENT TENURE AND PERFORMANCE OF EUROPEAN COMPANIES

Закажите новую по вашим требованиям

Представленный материал является образцом учебного исследования, примером структуры и содержания учебного исследования по заявленной теме. Размещён исключительно в информационных и ознакомительных целях.

Workspay.ru оказывает информационные услуги по сбору, обработке и структурированию материалов в соответствии с требованиями заказчика.

Размещение материала не означает публикацию произведения впервые и не предполагает передачу исключительных авторских прав третьим лицам.

Материал не предназначен для дословной сдачи в образовательные организации и требует самостоятельной переработки с соблюдением законодательства Российской Федерации об авторском праве и принципов академической добросовестности.

Авторские права на исходные материалы принадлежат их законным правообладателям. В случае возникновения вопросов, связанных с размещённым материалом, просим направить обращение через форму обратной связи.

📋 Содержание

Chapter 1. Private Equity Funds 8

1.1. Private Equity Fund Structures 9

1.1.1. Private Equity Fund Classifications 9

1.1.2. Private Equity Legal Structures 9

1.2. Private Equity Fund Life Cycle 10

1.3. Value Creation for Private Equity Portfolio Firms 15

1.4. Private Equity Exit Routes and Risks 17

1.4.1. Private Equity Exit Strategies 17

1.4.2. Private Equity Risks 18

1.5. Private Investment in Public Equity 19

1.5.1. Strengths and Weaknesses of PIPEs 20

Summary 22

Chapter 2. Private Equity Investment Tenure 23

2.1. Private Equity Investment Holding Period 26

2.1.1. Private Equity Investment Tenure Impact on Portfolio Firm’s Performance 26

2.1.2. Tenure of Leveraged Buyouts and Probability of Their Reversals 28

2.2. Private Equity Presence and Performance of Firms 30

2.2.1. Private Equity Investment Impact on Industry Performance 30

2.2.2. Impact of Private Equity Investments on Listed Equity 31

2.2.3. Private Equity Financing Impact on Firm Activities 32

Summary 34

Chapter 3. Empirical Study of the Relation Between Private Equity Investment Tenure and

Performance of European Companies 35

3.1. Research Hypotheses 35

3.2. Research Methodology 38

3.2.1. Variables 38

3.2.2. Sample Description 42

3.2.3. Descriptive Statistics 46

3.3. Empirical Results and Discussion 54

3.3.1. Determinants of Private Equity Investment 55

3.3.2. Investment Tenure Relation to the Performance of Target Companies 58

Conclusions 64

List of References 66

Appendix 1. List of Companies Used 70

📖 Введение

As a result, there is a number of positive outcomes of private equity investments. For example, company performance increases as PE funds improve existing management practices and supervise resources allocation. Greater innovation as private equity funds finance new research and development projects as well as young and innovative firms. The positive impact of PE on the performance of their investees in terms of their profitability and growth also translate into improvements in overall competitiveness of particular companies and industries as a whole.

As a consequence, private equity essentially contributes to economic growth. At the same time, PE funds are notorious for exceptional realized returns on their transactions. For instance, Nordic Capital’s 3-year investment in Nycomed (pharmaceuticals company based in Switzerland) granted the fund an unprecedented 74% gross return on investment. Another example of a transaction involves Lux Med (health care services company based in Poland) buyout. A landmark 1,000% gross return has been earned by Mid Europa Partners fund on this 6¬year long transaction.

The key question that raises is what factors drive private equity investment strategies that make such outstanding returns possible? What approaches do they use to determine their investee firms? Why would a PE fund choose to invest for 3 years in one company and twice as much in another? What is the impact of such investments on a portfolio company? Is there any relation between the investment tenure and the performance of investee?

Thus, the goal of this paper is to determine whether the tenure of private equity investments in European companies has relation to their performance. In order to achieve the specified goal, the paper will strive to provide new approaches in answering the above¬mentioned questions through a number of research goals:

• To conduct a study of private equity funds’ activities and their investment strategies.

• To analyze the possible causes of different investment strategies used by private equity funds, including different tenures.

• To conduct an empirical study in order to examine the relationship between private equity investments’ tenure and companies’ performance.

• To analyze the obtained results, formulate conclusions and practical recommendations based on the research.

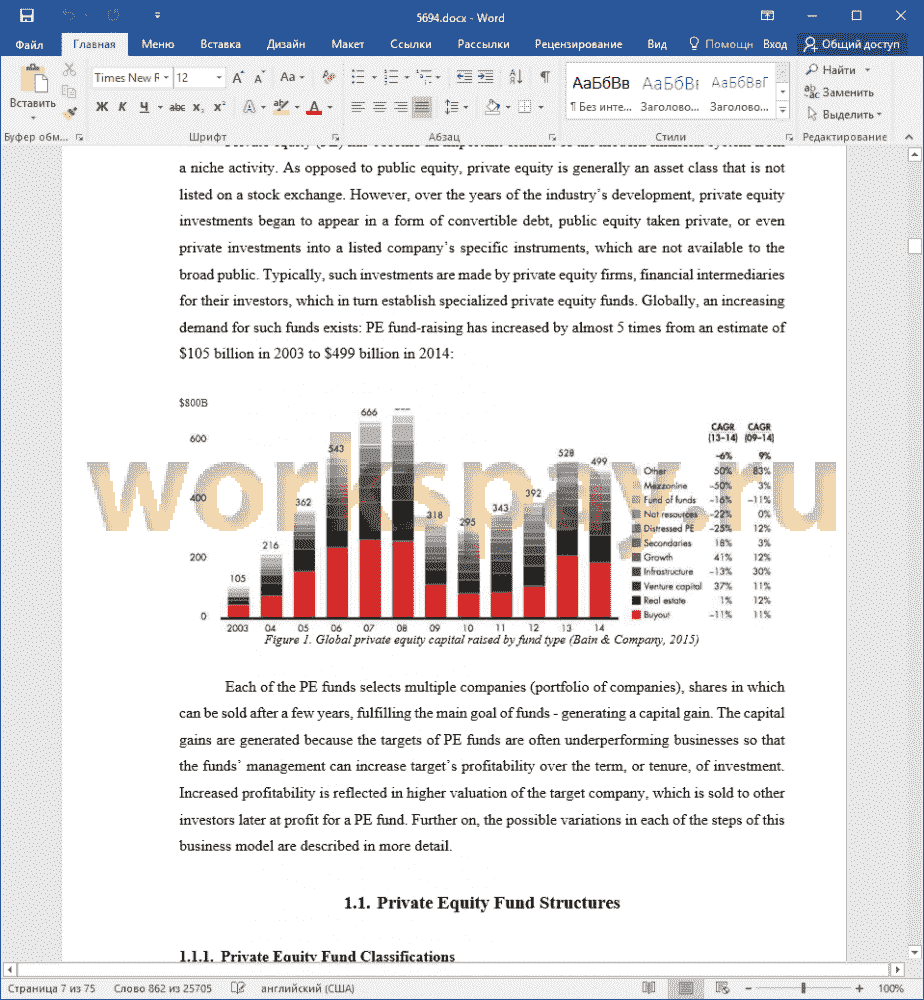

The paper will particularly focus on private investment in public equity (PIPE) transactions executed by PE funds. Within such transaction, a qualified investor buys a share in a listed company that wishes to raise capital in a cost- and time-efficient manner, as compared to seasonal equity offerings (SEOs). This effectiveness is achieved because PIPEs have a number of benefits over other methods of equity financing: PIPEs do not require immediate regulatory registration of the equity issue, do not need expensive roadshows while placement agents’ fees are lower than such of underwriting banks. These features have made PIPE transactions increasingly attractive in the recent years: in 2015, an increase of 38.7% in global capital raised through PIPEs and total market size of $85.7 billion could be observed (PrivateRaise, 2016).

The paper structure is following: the first chapter is devoted to the study of private equity activities and investment strategies. This chapter also focuses on peculiarities of PIPE transactions. The second chapter analyzes the possible causes of different investment strategies of PE funds. This chapter also addresses theoretical approaches, which describe the relationship between PE investment tenure or presence in general and performance of the portfolio firms. The third chapter is dedicated to the empirical study of the relationship between private equity investment tenure and performance of the target companies. This chapter also covers all the steps of the empirical research: its methodology, results of econometric and statistical analysis, discussion of main findings, as well as practical recommendations.

The paper also applies several theoretical concepts covered in existing academic research. For instance, research methodology draws particular ideas from “Determinants of Private Equity Investment in European Companies” paper of Badunenko, Barasinska, Schafer (2009) and “Access to Private Equity and Real Firm Activity: Evidence from PIPEs” paper of Brown and Floros (2012).

The empirical part of the paper is based on a sample of PIPE transactions that took place in the years 2005 - 2014 and had European target companies. The sample is based on transaction, financial, and shareholder structure information acquired from Thomson Reuters Eikon and Datastream databases.

Main findings of the paper extend currently available research of both PIPE transactions and private equity by introducing several approaches, which were not previously covered in academic papers. What is more, practical recommendations of the paper are useful for both the firms, which consider PIPE financing, and for private equity investment decision-making.

✅ Заключение

Second, possible causes of different investment strategies used by private equity funds, including different tenures, have been analyzed. In respect of investment tenures, type of transaction and target investee characteristics might matter the most. For PIPE transactions, a predominant group of issuers has been identified as high-tech companies that are comparably small in size and that experience difficulties with access to other sources of capital, such as debt (Brown and Floros, 2012; Sarve, 2013, p. 31). The failure to raise capital elsewhere could also be attributed to inability to meet the imposed bank loan maintenance covenants, such as Debt / EBITDA, which is also used by rating agencies as one of core ratios to determine the credit rating of a bond issue on debt capital markets (Standard & Poor’s Financial Services, 2013). Most of PIPE transactions have also been discovered to involve minority investments with lack of control over investees (Fraser-Sampson, 2007, p. 49; Sarve, 2013, p. 32) and that targets of such investments are frequently financially distressed enterprises (Dai, 2011). The above¬mentioned findings imply that private equity tenure, on average, might be equal to the time needed for companies to exit the distressed state and improve their financial performance to be able to raise capital from other sources. In case such improvements are not likely to take place, a fund might choose to exit immediately.

Third, an empirical study has been conducted in order to examine the relationship between private equity investments’ tenure and companies’ performance. The sample of 91 PIPE transactions corresponding to 79 European target companies that occurred from the year 2005 to 2014 has been used. The sample has revealed findings, similar to those discussed before: prevailing targets of PIPEs are small- and medium-sized enterprises, many of which are financially distressed. Also, a supplementary study associated with the determinants of private equity investments has been conducted.

Fourth, the obtained results have been analyzed and conclusions have been formulated based on the research. The study regarding the determinants of private equity investments revealed that less risky companies with comparatively higher financial leverage are more likely to attract private equity investors (ceteris paribus). No conclusions on the relation between the companies’ profitability and the likelihood of becoming a target of PIPE investment could have been made. In respect of the investment tenure, positive relation to the companies’ performance has been discovered, both in terms of their cash flow growth and solvency (as measured by net financial debt to EBITDA ratio).

The fact that companies with comparatively higher financial leverage are more likely to attract PIPE investors implies that targets with a greater track record of debt repayments are chosen for the transaction. Thus, improvements in their solvency might be desirable. Nevertheless, such companies, still, are mostly equity-financed, which is also in line with the assumption that those are unable to attract other sources of capital. Over the private equity tenure, however, either debt or other forms of equity markets should become more reachable for the companies as the solvency improves.

What is more, the paper provides practical recommendations based on the research. Even though there are almost immediate increases in companies’ capability to repay debt and growth rates of their cash flows, such are not observable for the tenures beyond 6 years. The exhausted potential to improve solvency and cash flow growth implies that private equity funds, on average, should consider either providing additional capital to the company or sell its share. From the company’s perspective, the recommendations are similar: were the solvency improvements not sufficient to increase access to debt markets, raising additional capital through a PIPE should be considered. This recommendation is in line with current practice of recurring PIPE investments in the same target companies.

Thus, the goal of the paper has been achieved: the relationship between the tenure of private equity investments and the performance European companies has been determined. The research, however, might be expanded in certain ways. First, the investment tenure relation to other practice-oriented characteristics might be considered. Especially, this is the case for various multiples used in the comparable company and transaction valuation, which are also applied by private equity funds to estimate their exit price. Second, the research might be extended for other types of private equity transactions as long as the tenures of specific investors are analyzed.

📕 Список литературы

🖼 Скриншоты