Тема: THE ROLE OF CORPORATE GOVERNANCE IN MERGERS AND ACQUISITIONS: HOW BOARD STRUCTURE AFFECTS M&A PERFORMANCE

Закажите новую по вашим требованиям

Представленный материал является образцом учебного исследования, примером структуры и содержания учебного исследования по заявленной теме. Размещён исключительно в информационных и ознакомительных целях.

Workspay.ru оказывает информационные услуги по сбору, обработке и структурированию материалов в соответствии с требованиями заказчика.

Размещение материала не означает публикацию произведения впервые и не предполагает передачу исключительных авторских прав третьим лицам.

Материал не предназначен для дословной сдачи в образовательные организации и требует самостоятельной переработки с соблюдением законодательства Российской Федерации об авторском праве и принципов академической добросовестности.

Авторские права на исходные материалы принадлежат их законным правообладателям. В случае возникновения вопросов, связанных с размещённым материалом, просим направить обращение через форму обратной связи.

📋 Содержание

CHAPTER 1. THE BOARD STRUCTURE AND M&A PERFORMANCE 10

1.1 Theoretical context: mergers and acquisitions (M&A) 10

1.2 Corporate governance and M&A deals 12

1.3 Hypotheses formation 15

1.4 Mergers and acquisitions: performance measurement 20

1.5 Effects of industry specifics on value creation from M&A 24

CHAPTER 2. EMPIRICAL STUDY OF THE RELATIOSHIP BETWEEN THE BOARD

STRUCTURE AND M&A PERFORMANCE 27

2.1 Research goals and questions 27

2.2 Sample selection and data collection 27

2.3 Methodology 28

CHAPTER 3. FINDINGS AND DISCUSSION 35

3.1. CAR characteristics on event windows 35

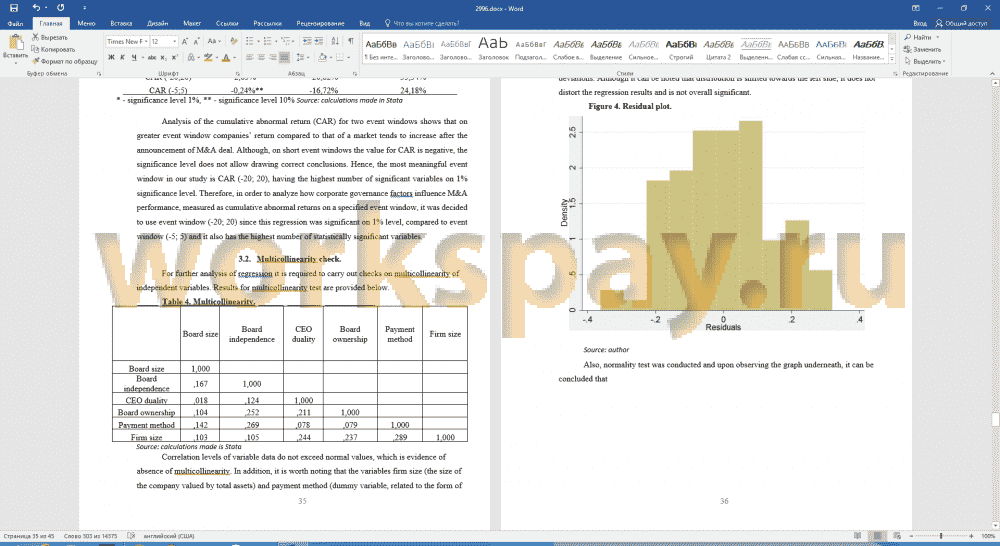

Upon conducting analysis of cumulative abnormal returns for event windows (-20; 20) and (¬5; 5) the following data has been received, which is shown in the table below 35

3.2. Multicollinearity check 35

3.3. Analysis of residuals and normality test 36

3.4. Regression analysis 37

CHAPTER 4. SUMMARY AND DISCUSSION 39

4.1 Summary 39

4.2 Limitations and recommendation for further research 39

4.3 Implications for theory and practice 40

CONCLUSION 41

References 42

📖 Введение

There are two broad reasons for the companies to chose the strategy of M&A. The first and most common motive is expected synergies and efficiency gains, mainly the creation of value. The second motive arises from pursuing personal benefits from the acquisition of target firms. M&A deals which are in line with the second motive do not create value for shareholders, and can even destroy value.

Therefore, the main aim of this master thesis is to investigate a relationship between the structure of the board of directors and the operational performance of the firms following the M&A deal. In order to achieve this goal, this study has the following objectives:

• Make an analysis of previous studies to discover linkages between board characteristics and M&A performance

• Conduct an empirical study in order to point out the specific board characteristics which have significant effects on the cumulative abnormal returns of the firm around M&A

• Provide research and managerial implications

Choice of the industry

The current research is focused on the companies from pharmaceutical industry that can be explained by the following reasons:

1. The industry is global in nature and engages in M&A activity extensively. According to analysts, by 2020 the volume of the global pharmaceutical market will double to $ 1.8 trillion, which makes the sector particularly attractive for all players in this market (PwC Report, 2016).

2. The global nature of the industry means that findings of the researches considered pharmaceutical industry have broad applicability and can be widely used by different representatives of this industry.

3. For the last years the amount of M&A deals and their monetary value between companies from pharmaceutical industry have dramatically increased. According to Global M&A Report Pharma / Biotech 2015, the cumulative total transaction volumes of M&A deals of companies from pharmaceutical industry more than doubled in 2014 year in comparison with 2013. This fact proves the relevance of the topic in the present moment.

4. Quantity of researches dedicated to connections between M&A and corporate governance of the companies is increasing but still limited. Therefore, studies related to this topic will significantly contribute the existent pool of knowledge.

Structure of the paper

The study has the following structure. The first chapter of the thesis is dedicated to the academic literature overview. In this chapter there is an analysis of theoretical perspectives on the relationships between board of directors and M&A performance, together with the explanation of the agency theory, which is inherent in this type of transactions. Also, the hypotheses formulation will be based on the findings discussed in this section. The content of the second chapter is related to empirical study and includes methodology, description of the data, together with sources, variables description, regression analysis and finally results and following discussion. The third part includes analysis of the results. And finally, fourth part consists of discussions, suggestions for the future researches and recommendation for managers about implementation of the results on practice.

The findings of the study will be highly valuable not only for researchers, but also for practitioners. There will be provided managerial implications based on results of the study, providing recommendations to the managers with respect to the most appropriate board structure for the following M&A deal.

This study contributes to the theoretical knowledge base by providing an analysis of operational performance of the companies not from the market based perspective, but rather from operational side, which is not well researched area by far.

The overview of theoretical literature in this chapter is based on international scientific publications in well known, credible academic journals on finance, economics, and corporate governance. In order to gather data for empirical part, such databases as Thomson Reuters One and ZEPHYR have been used.

✅ Заключение

The statistical analysis helps to investigate that the most influential component of board structure that is positively related to M&A is independence of board of directors. It can be explained by the fact that independent board members usually significantly enhance companies’ monitoring activities that positively impacts decision-making process.

Regarding to board size, the results of the analysis have shown that the number of board of directors and M&A performance are inversely related. Large boards of directors consist of people with different backgrounds and views. These factors can cause communication and coordination problems, lead to misunderstanding and conflicts that significantly complicates process of decision-making.

Regarding to CEO duality, the statistical analysis has shown that the efficiency of M&A deals for companies, where there is a CEO duality, is lower than for companies, where there is no CEO duality. It can be explained by the reason that separation of the post of CEO and chairman of the board of directors in the company-acquirer leads to more objective assessment of the proposals of the transaction and mitigates the agency problem.

Finally, it was found that ownership by members of board of directors is not significant with respect to the performance of M&A deals and therefore the last hypothesis was not confirmed while others were.

To sum up, the current study reinforced the opinion that board of directors can become the strong point of the company that helps it to achieve corporate and economic goals and improve M&A performance as well.

📕 Список литературы

🖼 Скриншоты