Тема: The influence of environmental disclosures on the stock market in oil and gas sector

Закажите новую по вашим требованиям

Представленный материал является образцом учебного исследования, примером структуры и содержания учебного исследования по заявленной теме. Размещён исключительно в информационных и ознакомительных целях.

Workspay.ru оказывает информационные услуги по сбору, обработке и структурированию материалов в соответствии с требованиями заказчика.

Размещение материала не означает публикацию произведения впервые и не предполагает передачу исключительных авторских прав третьим лицам.

Материал не предназначен для дословной сдачи в образовательные организации и требует самостоятельной переработки с соблюдением законодательства Российской Федерации об авторском праве и принципов академической добросовестности.

Авторские права на исходные материалы принадлежат их законным правообладателям. В случае возникновения вопросов, связанных с размещённым материалом, просим направить обращение через форму обратной связи.

📋 Содержание

ABSTRACT 4

INTRODUCTION 5

LITERATURE REVIEW 6

THEORETICAL FOUNDATION 13

METHODOLOGY 16

research design 16

data collection process 18

methods and data description 19

RESULTS 22

CONCLUSION 27

REFERENCES 30

APPENDIX 33

📖 Введение

Originally, the environmental disclosures were part of ESG (Environmental, Social and Governance) practices designed to estimate the performance of a public company from the perspective of the principles of sustainable development and business ethics. These practices became more relevant during the last years which motivated public companies to accumulate and allocate relevant data to be presented to shareholders and potential investors (Lin, J., & Qamruzzaman, M., 2023). Thus, at the current moment there is no defined and confirmed link between sustainability reports and market reaction.

The main questions standing behind this work are “Why do companies spend resources to present sustainability data?” and “How does this sustainability data influence the stock market?”.

Therefore, the research question is following: “What is the influence of environmental disclosures published by public companies in the oil and gas sector on the quantitative characteristics of the stock market?”

Nowadays there is a lot of skepticism regarding the impact of sustainability reporting and such kind of activity may be considered controversially by market participants. The primary goal of the research is to define the market reaction on the environmental disclosures published by companies in the oil and gas sector. It implies both the short-term and long-term impact of the sustainability reports on the expected return of the stock. The expected results will increase the predictive power of the financial models estimating the attractiveness of different companies on the stock market. If the stated hypotheses are approved, the empirical analysis may decrease the uncertainty existing on the market and provide more instruments to estimate a company's long-term capacity. The main challenge in this case is that there is no defined structure for the sustainability reports approved, which makes the comparison more difficult. Nevertheless, there is a list of indicators which are presented by the majority of public companies. These indicators are greenhouse gas emissions, water consumption, waste disposal and air pollution. All the mentioned factors have a sufficient influence on the environment and, what is more, they all are related to the operational processes of companies operating in the oil and gas sector. This sector is a major contributor to greenhouse gas emissions, which are a leading cause of climate change. By monitoring and reducing these emissions, the sector can mitigate its environmental impact and contribute to global efforts to combat climate change due to the fact that many countries have strict regulations governing the environmental impact of oil and gas operations. Companies in this sector must adhere to these regulations to avoid fines and penalties, as well as maintain their social license to operate (Qintharah, Y. N., & Utami, F. L., 2023). At the same time, consumers and investors are increasingly concerned about the environmental impact of the companies they support. By demonstrating a commitment to reducing greenhouse gas emissions, water consumption, waste disposal, and air pollution, oil and gas companies can improve their public perception and protect their reputation. So, there are many factors which support the assumption that different agents, both external and internal ones, are aware of the environmental disclosures and may act differently depending on the data presented. Therefore, the final version of the research goal is to quantitatively represent short-term and long-term changes occurring on the stock market in the oil and gas sector as a result of publication of environmental disclosures.

✅ Заключение

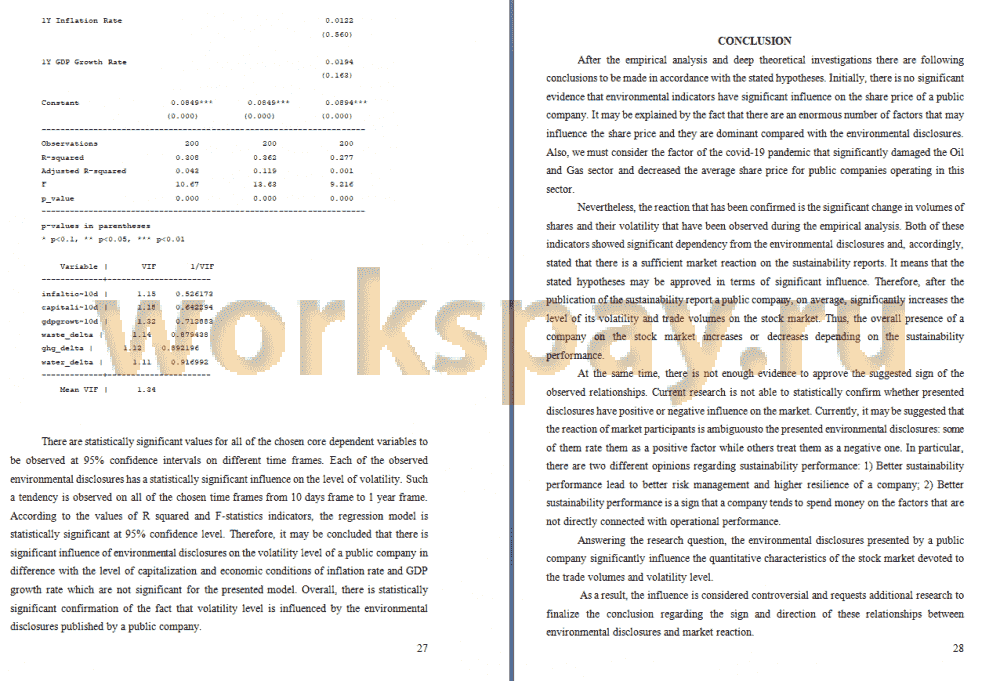

Nevertheless, the reaction that has been confirmed is the significant change in volumes of shares and their volatility that have been observed during the empirical analysis. Both of these indicators showed significant dependency from the environmental disclosures and, accordingly, stated that there is a sufficient market reaction on the sustainability reports. It means that the stated hypotheses may be approved in terms of significant influence. Therefore, after the publication of the sustainability report a public company, on average, significantly increases the level of its volatility and trade volumes on the stock market. Thus, the overall presence of a company on the stock market increases or decreases depending on the sustainability performance.

At the same time, there is not enough evidence to approve the suggested sign of the observed relationships. Current research is not able to statistically confirm whether presented disclosures have positive or negative influence on the market. Currently, it may be suggested that the reaction of market participants is ambiguous to the presented environmental disclosures: some of them rate them as a positive factor while others treat them as a negative one. In particular, there are two different opinions regarding sustainability performance: 1) Better sustainability performance lead to better risk management and higher resilience of a company; 2) Better sustainability performance is a sign that a company tends to spend money on the factors that are not directly connected with operational performance.

Answering the research question, the environmental disclosures presented by a public company significantly influence the quantitative characteristics of the stock market devoted to the trade volumes and volatility level.

As a result, the influence is considered controversial and requests additional research to finalize the conclusion regarding the sign and direction of these relationships between environmental disclosures and market reaction.

Also, it is necessary to address the potential limitations of the research that should be considered to increase the relevance of the work. Firstly, the main theoretical limitation is the huge amount of potential variables that potentially affect the stock market. Different types of economic, social and political factors have direct influence on the stock market and, accordingly, on the research that has been done. Secondly, the choice of environmental disclosures may not be optimal. On average, each public company presents more than 25 environmental disclosures which may have a stronger influence on the market and be considered by a higher share of market participants. Finally, working with secondary data implies the presence of an endogeneity problem: there is no 100 % probability that the data of environmental disclosures has been collected and accumulated without bias and errors.

📕 Список литературы

🖼 Скриншоты