Тема: The relationship between corporate social responsibility disclosure and financial performance of Russian companies

Закажите новую по вашим требованиям

Представленный материал является образцом учебного исследования, примером структуры и содержания учебного исследования по заявленной теме. Размещён исключительно в информационных и ознакомительных целях.

Workspay.ru оказывает информационные услуги по сбору, обработке и структурированию материалов в соответствии с требованиями заказчика.

Размещение материала не означает публикацию произведения впервые и не предполагает передачу исключительных авторских прав третьим лицам.

Материал не предназначен для дословной сдачи в образовательные организации и требует самостоятельной переработки с соблюдением законодательства Российской Федерации об авторском праве и принципов академической добросовестности.

Авторские права на исходные материалы принадлежат их законным правообладателям. В случае возникновения вопросов, связанных с размещённым материалом, просим направить обращение через форму обратной связи.

📋 Содержание

CHAPTER 1: THEORETICAL ASPECTS OF CORPORATE SOCIAL RESPONSIBILITY 7

1.1 The concept of corporate social responsibility 7

1.2 Approaches to measuring corporate social responsibility 12

1.3 The relationship between CSR and financial performance 14

1.4 Peculiarities of CSR in Russia 18

1.5 Hypotheses statement 22

CHAPTER 2: EMPIRICAL ASSESSMENT OF RELATIONSHIP BETWEEN CSR

DISCLOSURE AND CORPORATE PERFORMANCE 25

2.1 Sample 25

2.2 Research methodology 26

2.3 Variables' description and data collection technique 28

2.4 Descriptive statistic 33

2.5 Regression models' estimation 36

2.5.1 Correlation analysis 36

2.5.2 Ohlson model estimation 37

2.5.3 Estimation of basic CSR index 38

2.5.4 Estimation of extended CSR index 41

2.5.5 Estimation of models with control variables 42

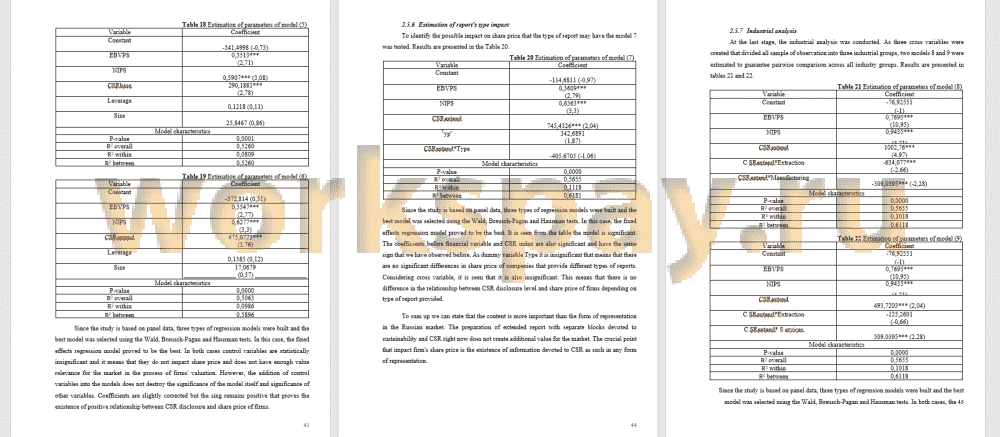

2.5.6 Estimation of report's type impact 44

2.5.7 Industrial analysis 45

2.6 Managerial applications 47

CONCLUSION 49

APPENDIXES 51

Appendix 1 List of companies included in the sample 51

Appendix 2 Distribution of level of disclosure of basic index 54

Appendix 3 Distribution of level of disclosure of extended index 55

Appendix 4 Distribution of levels of disclosure of all indicators 56

REFERENCES 57

📖 Введение

The question of CSR disclosure value relevance aroused the interest of researchers and practitioners and gave rise to various theories on this subject. On the one the formation and evolution of stakeholder theory and its instrumental aspects in particular has provided the foundation that CSR can help in building and solidifying trusting relationships with a variety of constituents (employees, consumers, local communities, environmental activists and concerned citizens among many others) that are important to the firm's long-term success and financial standing. According to this approach it is important for companies to invest in such activities and provide results to the stakeholders.

On the other hand, CSR activities are mainly not connected directly with core firm's activities and even might restrict some business processes and as a result limit the possibilities for future growth. It leads researchers to the opinion that CSR imposes an unjustified and fundamentally undemocratic taxation on shareholders, that its implementation costs outweigh any potential tangible benefits and that due to this, it constitutes a misallocation and misappropriation of valuable company resources. As a result, the positive contribution of CSR disclosure to the firms' market value cannot exist.

Even though various stakeholders (investors, clients, regulators, employees, etc.) demand greater transparency of companies' CSR activities, and CSR disclosure is gradually becoming an integral part of annual reports, the exact answer to the question of whether there is a relationship between CSR disclosure and market prices still does not exist. Researches conducted in this field do not provide definite position and sometimes even have opposite results. Such kind of discrepancy arises from lack of common understanding of CSR activities and approaches to its estimation as well as various research designs. So, the topic has a high potential for the contribution to the theoretical basis in the field.

From practitioners' point of view it is also important to understand the relationship between CSR disclosure and share price performance. We can identify at least two areas where this understanding might be useful: preparation of integrated reports and investment decision making. As for investment decision making managers should understand what return will give available projects. In case with some environmental and/or social projects or programs it is rather difficult to calculate because they may not generate additional cash flows. The market reaction on investing in CSR activities might be the measure of return of such projects and as a result become the basic line for decision making process. Speaking about preparation of integrated reports it is important to mention that it consists of many blocks of different information, has obligatory and voluntary parts. However, these blocks might have the different value relevance for the market. Moreover, the value relevance might differ depending on firm's industry. Understanding of such pattern may help managers to create the efficient way of report preparation: they can understand what block they should focus on, in what type of information investors are interested in, what voluntary disclosure is valuable and what one is not worth the efforts because it is not create any additional value. So, it can be seen that the understanding of relationship between CSR disclosure and share price performance can help managers to allocate resources to the projects and plan the working process in the most efficient way.

Research goal of this study: To determine the relationship between CSR disclosure and firms’ market value.

...

✅ Заключение

Review of existing literature in this field found out that the investigation of the relationship between CSR disclosure and firm's market value remains actual and interesting for the recaches during several last decades. But due to difficulties of identification CSR definition and absence of one common approach to CSR estimation results of various researchers significantly differ. However, the majority supports the idea that CSR disclosure may positively impact market indicators of the company.

Based on the theoretical basis of corporate social responsibility concept and reseaches that were made previously the following hypotheses were formulated for this study:

H1: There is a positive relationship between level of basic CSR disclosure and share price of firms

H2: There is a positive relationship between level of extended CSR disclosure and share price of firms

H3: There is a difference in relationship between level of extended CSR disclosure and share price of firms among extraction companies, manufacturing companies and services companies.

The study was conducted on the Russian market in several stages. Main trends in CSR development in Russia and Russian peculiarities of non-financial reporting devoted to CSR is investigated. At the empirical part of the work, firstly the classical Olson linear model was evaluated, which formed the basis for further identification of the relationship between the level of CSR disclosure and the share price. Five different blocks of CSR activities were considered, and two types of CSR index were proposed one. Basic index included the most used indicators from environmental and social blocks. Extended index consisted of wider range of indicators.

Mean-comparison tests and estimation of regression models with basic and extended CSR indices showed that there is a relationship between the level of CSR disclosure and companies' share price. This relationship is positive, and the increase of CSR disclosure may lead to improvement of market performance. As the relationship is significant and positive in both cases (with basic index and with extended one) we may state that all blocks of information are important for the market and companies should be involved in such many CSR projects as possible and demonstrate it to the stakeholders.

Then to check models for robustness with help of control variables were added to models and there were no destruction of models and significant changes of coefficients. So, both hypotheses H1 and H2 were accepted. Additional analyses of possible impact of report's type on the market result and importance of CSR disclosure is conducted. It is concluded that type of report does not impact any results of model previously estimated and insignificant for the market.

Industrial analyses showed that in current situation CSR disclosure plays more important role for the services companies while there are no differences in the relationship between CSR disclosure and firms’ market value between extraction and manufacturing companies. It is supposed that such result is caused by Russian specifics of CSR reporting and might be temporary. As a result, H3 was partially accepted.

Based on the obtained results it can be stated that CSR disclosure in annual reports has value relevance for the market, that is why managers should prepare the plan of CSR activities, carefully analyze investment projects in the field of CSR and their possible return and present their results and future plans in annual reports. For investors CSR disclosure might become the indicator of companies' development stage and estimation of its success and may help to find out the most interesting securities that will be included into their portfolio. As for government and authorities, they should improve the controlling and regulating function in the field of CSR to contribute to the development of CSR practices and their implementation into corporate strategy.

Summing up, we can say that all the hypotheses put forward were tested, the goal of the work was achieved. A further direction of this study could be the investigation of value relevance of separate blocks of CSR index and the transition to a purely quantitative CSR index and the identification of its potential impact on the firm's market performance.

📕 Список литературы

🖼 Скриншоты