Тема: Accounting-based modelling for bankruptcy prediction for privately-held small and medium manufacturing companies: the case of Italy

Закажите новую по вашим требованиям

Представленный материал является образцом учебного исследования, примером структуры и содержания учебного исследования по заявленной теме. Размещён исключительно в информационных и ознакомительных целях.

Workspay.ru оказывает информационные услуги по сбору, обработке и структурированию материалов в соответствии с требованиями заказчика.

Размещение материала не означает публикацию произведения впервые и не предполагает передачу исключительных авторских прав третьим лицам.

Материал не предназначен для дословной сдачи в образовательные организации и требует самостоятельной переработки с соблюдением законодательства Российской Федерации об авторском праве и принципов академической добросовестности.

Авторские права на исходные материалы принадлежат их законным правообладателям. В случае возникновения вопросов, связанных с размещённым материалом, просим направить обращение через форму обратной связи.

📋 Содержание

CHAPTER 1. THEORETICAL BACKGROUND 7

1.1 Examination of manufacturing SMEs in Italy: the issue of bankruptcy 7

1.2 Definition of bankruptcy 9

1.3 Bankruptcy prediction: Accounting-based models 10

1.4 Bankruptcy prediction: Tools 19

CHAPTER 2. METHODOLOGY 23

2.1 Statistical methodology 23

2.1.1 Logit specification 23

2.1.2 Models specification 24

2.1.3 Prediction quality assessment 27

2.2 Sample collection 29

2.3 Sample description 32

CHAPTER 3. RESULTS AND MANAGERIAL IMPLICATIONS 35

3.1 Results 35

3.2 Limitations 42

3.3 Managerial Implications 43

CONCLUSION 45

LIST OF REFERENCES 47

APPENDIX 59

Appendix 1. Correlation matrix 59

Appendix 2. Youden index 60

📖 Введение

As mentioned by Bal (2016), bankruptcy is often a long-term process that starts several years prior to the undesired event and the earlier companies gain insights on their position, the more chances they have to rectify the situation and avoid bankruptcy declaration. Most of the time, it does not happen the way that companies are operating and, suddenly, declare bankruptcy. Before a company files bankruptcy, it has an ability to get additional financing from banks. However, it is also a challenging task. After the global financial crisis in 2008, Basel Committee of Banking Supervision (BCBS) issued the third edition of Basel requirements for banks, that imposed more restrictions on banks in terms of leverage and liquidity in order to decrease the risks for banks and make them not so vulnerable to large financial instabilities (Bank for international settlements, n.d.). As a result, banks are now reluctant to give additional loans to companies that are in danger. That is the reason why it is necessary for companies to recognize the signals of upcoming problems before it is too late.

First attempts to address the issue have been made in 1930th (Bureau of business research, 1930). Since then, researchers have been trying to elaborate on a methodology that will be capable of making accurate predictions of bankruptcy several years prior to the event. If working, such methodologies could be used by creditors for assessment of companies, by suppliers and buyers to assess risks and by companies themselves to foresee their default and make an action in case there are impending problems. The first model that came into place was introduced by Beaver (1966). Later on, there has been a surge in the development of various models with the use of different statistical techniques and indicators. Much attention has been put to the research of Ohlson (1980), Zmijewski (1984) and Altman (1968), since the models introduced in these papers have proved to be effective for the task of bankruptcy prediction across several countries. However, the note should be made regarding the adaptability of every bankruptcy prediction model to varying conditions. There is no unique bankruptcy prediction model that will suit all the countries, economic conditions and industries. When comparing the effectiveness of the same model on varying circumstances, researchers tend to come to different results. Hence, the majority of bankruptcy prediction models produce varying classification accuracy rates for different samples. The contradiction has been found in the research of Du Jardin and Sdverin (2012), Tsai and Cheng (2012), Bansal & Kashyap (2020) and Seto (2022). The difference in results creates the need to find an appropriate model for each country, industry and economic situation separately.

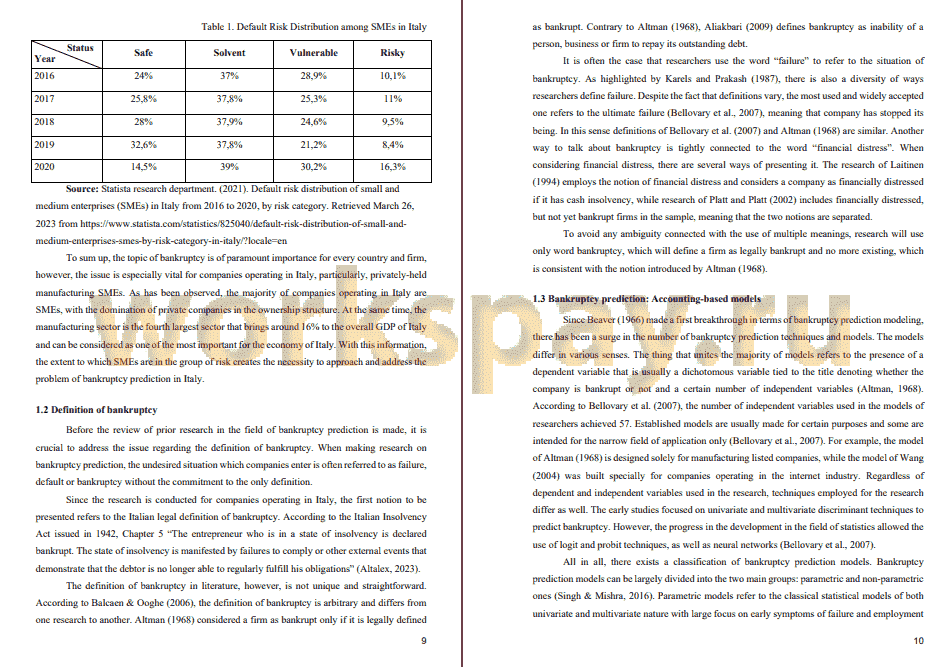

The research will focus on the case of bankruptcy prediction of privately-held small and medium manufacturing enterprises operating in Italy. The choice has been made in favor of small and medium enterprises (also referred to as SMEs) due to the fact that SMEs account for 99% of Italian service and industrial firms (OECDiLibrary, 2020). At the same time, the percentage of vulnerable companies and companies at high risk of bankruptcy category among SMEs was equal to 46,5% of all SMEs as of 2020, which is a 57% increase as compared to 2019 (Statista Research Department, 2021). Hence, the issue of bankruptcy prediction in Italy is of paramount importance.

Before considering the research gap that has been formulated after detailed literature review, it is worth mentioning two factors. First, there are numerous models that were built by researchers to forecast bankruptcy; however, the primary emphasis of these models is on the application to public companies. At the same time, the importance of bankruptcy prediction for private companies cannot be underestimated but the literature researching this topic is quite limited (Matenda et al., 2021). It especially refers to Italian SMEs, where the number of private companies is prevalent (OECDiLibrary, 2020). Second, the business environment is different across countries, which results in the effectiveness of some models, and at the same time total uselessness of other models. Platt and Platt (1990) confirm that the differences in economic environment are likely to change the relationship between dependent and independent variables, the range of independent variables and the relationships among the independent variables. In addition, Grice and Ingram (2001) state that structure of the models changes over time, as well as the importance of certain ratios, which requires the re-estimation of coefficients of the ratios in models. Summing up all the factors mentioned above, a research gap is formulated as follows: there is limited research regarding the bankruptcy prediction model suitable for privately-held small and medium manufacturing companies operating in Italy in current economic and business conditions....

✅ Заключение

The problem existed a long time ago and its relevance is only increasing with the growth of the number of enterprises. Every company is in need of a special framework or tool that could be deployed easily to predict bankruptcy as early as possible. Such tools could be used to realize that something goes wrong with a company's management. When management is aware of serious problems, the company is given a chance to survive and eliminate the vulnerabilities. The work on the bankruptcy prediction tools started in the 1930s and is still continuing. Great progress has already been achieved, however, one of the conclusions of the whole work refers to the need to validate existing models and/or develop new models for each and every economic, business condition and country.

The thesis has addressed the issue of bankruptcy for the special case of privately-held small and medium manufacturing enterprises operating in Italy. Such a narrow object was chosen due to the research gap associated with such a group of enterprises, which are undoubtedly crucial and central to the economy of Italy. To achieve the research goal the academic literature has been considered including the notion of bankruptcy according to the Italian law and works of various researchers, approaches to the prediction of bankruptcy, accounting-based models employed and results achieved among samples and statistical tools employed by researchers to build models.

The research compared the prediction quality of well-established models of Altman (1983), Ohlson (1980) and Zmijewski (1984) on the sample of privately-held manufacturing SMEs operating in Italy which was collected with ORBIS database. Then, the research combined the most recognized financial indicators to arrive at the combined model Q and compared the accuracy of the four models on the established sample. All the four models were built with the help of logistic regression as the statistical tool is considered as one of the most reliable ones and makes it possible to compare results produced by each of the models. Overall, the research goal has been achieved: the combined Q model was able to predict bankruptcy at the rate of 98.06% one year prior to bankruptcy. Hence, the research gap has been fulfilled because the solution for the niche of manufacturing companies operating in Italy has been found.

The research results create value for stakeholders in that it provides a simple tool for assessing the company that could be easily utilized by the company itself, investors, employees, buyers and suppliers without additional investments. The solution provides valuable insights regarding the state of the company nowadays and its possible development in the near future. Those insights could be considered by the mentioned groups of stakeholders to make informed decisions when entering relationships with the companies operating in the researched field.

📕 Список литературы

🖼 Скриншоты