Тема: DETERMENING THE SPECIALIZED CRITERIA FOR VALUATION OF STARTUPS AS A POTENTIAL INVESTMENT

Закажите новую по вашим требованиям

Представленный материал является образцом учебного исследования, примером структуры и содержания учебного исследования по заявленной теме. Размещён исключительно в информационных и ознакомительных целях.

Workspay.ru оказывает информационные услуги по сбору, обработке и структурированию материалов в соответствии с требованиями заказчика.

Размещение материала не означает публикацию произведения впервые и не предполагает передачу исключительных авторских прав третьим лицам.

Материал не предназначен для дословной сдачи в образовательные организации и требует самостоятельной переработки с соблюдением законодательства Российской Федерации об авторском праве и принципов академической добросовестности.

Авторские права на исходные материалы принадлежат их законным правообладателям. В случае возникновения вопросов, связанных с размещённым материалом, просим направить обращение через форму обратной связи.

📋 Содержание

Введение

FINANCE 10

1.1. Defenition and general information about Venture Finance 10

1.2. Investment process and stages of start - up financing 16

1.3. Investment criteria of Venture Funds 20

1.3.1. Reverse engineering research 22

1.3.2. Real life researches 26

1.4. Summary of the investment criteria 30

CHAPTER 2. EMPERICAL RESEARCH OF VENTURE CAPITAL FUNDS DECISION -

MAKING 34

2.1. Estimation of the parameters that influence a fundraising decision 34

2.2. Data and sample 40

2.3. Econometric analysis 43

2.4. Managerial applications 48

2.5. Limitations and further research 50

CONCLUSION 51

REFERENCES 53

📖 Введение

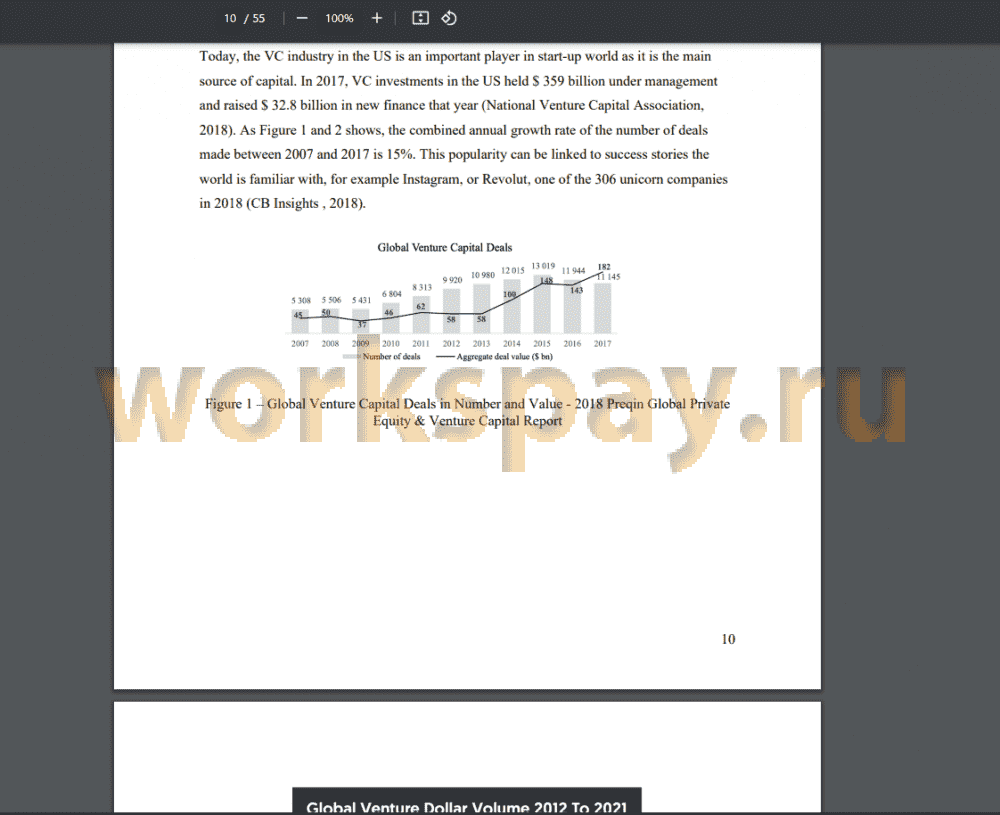

To do so, founders and companies need access to the capital required to establish and grow a successful business. However, small companies bear high level of uncertainty and risk. Hence, such companies often face difficulties with the access to the capital (Paul Gompers J. L., The Venture Capital Revolution, 2001). Traditional sources of capital, such as banks do not want to take such excessive risk and usually deny loans to start - ups or require high premiums for those loans. In the circumstances of unavailability of traditional sources of capital young companies can raise capital from Venture Capital funds (VCs) (Allen Berger, 1998). Venture capital is a source of capital and experience for young , innovative and promising companies that seek development and growth (National Venture Capital Association, 2018).

During the last 30 years venture capital had been one of main and an important source of capital for many start - ups (Paul Gompers W. G., 2016). Even though it has been estimated that in the US less than 1 % of new businesses receive venture capital, more than 60 % of initial public offerings (IPO) in the US are backed by venture capitalists (Steven Kaplan, 2010).

Frequently venture capital funds focus on one specific segment of the market where they have expertise, network of experts and know potential customers. Hence, VC funds could be considered industry experts and specialist in identifying the most promising start - ups for investment. This makes it particularly important to analyse the decision making process of venture investors and understand what parameters are they using to evaluate potential investments. This problem had received a lot of attention from the scholars in the last couple of decades (Tyzoon T. Tyebjee, 1984, Ian C.Macmillan, 1985, Vance H. Fried, 1994, Dan Muzyka, 1996, Andrew L.Zacharakis, 1998, Shepherd, 1999, Colin Mason, 2004, Jeffrey S. Petty, 2011, Josd Carlos Nunes, 2014). One of the reasons why it is important to understand the parameters used to evaluate investment opportunities is the possibility to predict the success of the start - up. Naturally, venture capitalists want to make profits on their investments and they want to invest in companies that will grow. Therefore, the criteria used in the decision making could be used to predict which companies will succeed and which will fail in the future. (Dean A. Shepherd, Venture capitalists' expertise: A call for research into decision aids and cognitive feedback, 2002). Secondly, clear list of parameters will help founders and entrepreneurs plan their fundraising campaigns and increase their probability of success. That would dramatically increase the number of SMEs as many business die in the first couple of months of their existence due to problems with capital (Nikolaus Franke, 2008). Lastly, a better understanding of the decision-making process of venture capitalists may improve the survival rates of startups and their growth rates (Andrew L.Zacharakis, 1998).

Analysis of the past studies shows that they tried to just identify the most important criteria but not to find their connections and correlations. Also, none of the previous studies attempted to create a clear list of those criteria used for the valuation of start - ups as an investment opportunities. Previous researches found that there could be up to 400 different criteria used in the due diligence process of the venture fund. So, many researches focused on the most relevant ones in such condition of overabundance of criteria (Tobias Kollmann, 2010). Their findings are somewhat intuitive. The top priorities for venture capitalists are management team, product, market and financial characteristics of the company under consideration. Still, it must be noted that there is no consensus in existing literature on the ranking of the four most important criteria

To sum up everything that was said before - venture investors decision making process is complicated and complex. Also the illiquid and long - term nature of such investments only adds complexity as it makes the relationship between the investor and the founder more dependant of each other (Vance H. Fried, 1994). In addition, venture capitalists face the worst choices and the moral risks of their investments. The risk of market failure due to asymmetry of information is higher in venture finances than in the traditional investment environment because venture investments are usually made in companies with very small tangible assets that they can offer as collateral and have no history that can improve their reputation. However, it has been argued that the existence of venture finance is defined by the ability of venture capitalists to reduce costs and risks from information asymmetries via various sources and instruments (Raphael Amit, 1998).

Clearly, venture capitalists face major challenges in their investment decisions, which in turn highlight the importance of the clear and structured investment decision-making process. Researches seemed to be aware of this. In a recent study, US-based investors have indicated that educational research on investment decisions is the second most relevant field of finance research after exit strategies (Mark V. Cannice, 2016). Perhaps the venture capitalists agree that they will still achieve the best practices: it has been argued that three of the four startups supported by businesses fail and will not bring profits to their investors (The Wall Street Journal, 2012). Undoubtedly, venture capitalists have room to improve their investment process. This requires further research into the investment decision-making process for venture capitalists, and investment criteria of VC is a part of it....

✅ Заключение

The hypothesises tested in this research are as follows:

H1: Venture funds use specific parameters to evaluate investment opportunities.

H2: Those parameters could be composed into universal scoring model.

H3: Out of all selected parameters there will be ones with the highest impact on the outcome. Team, Product properties and future Market will be the most important parameters.

H4: It is possible to model the decision - making process and predict or verify the result of evaluation of the VC fund.

Reviewing several studies in the first chapter of this paper, made it possible to name the most popular criteria of VCs to assess start - ups. They are management team, market size and dynamics, competitive position of the new product, deal parameters and financial characteristics of the start - up. That is, VCs evaluate the attractiveness of early-stage start - ups firstly by evaluating the competence and personal characteristics of the founders. VCs also evaluate the market potential of the venture and pay close attention to the venture’s financial characteristics.

Another very important parameter is the intuition. It plays an important part in VCs’ decision-making (Hisrich & Jankowicz 1990). However, it cannot be evaluated, measured or modelled. Some parameters are linked to the felling and intuition of the investor. Although, clear scoring parameters might help to minimize the influence of the intuition as they set a solid framework and almost fully eliminate the need to guess.

In order to check how this criteria, work a sample of 100 early - stage start - ups was analysed. This sample was provided by several Russia based VC funds along with their decisions about those companies. Companies from the sample are from the same fundraising stage, industry and time period. This made them as similar as possible and allowed to compare them. Parameters, chosen in the first chapter were described and justified, as well as their scoring rules. After they were determined, all 100 companies from the sample were scored to create a data sample for further analysis and modelling. Two models were created for the analysis: probit and linear regression model. Unfortunately, none of the models were precise enough to be used for forecasting of verification of the decision made by the fund. However, it was still possible to draw a conclusion about the importance of the parameters and select the most significant ones. After the analysis and modelling all 10 criteria were distributed into three groups with accordance to the results of the modelling. Six parameters were marked as significant, as they have the highest impact on the final investing decision. Three parameters were labelled important, as they can affect the significant ones and indirectly influence the final decision. Only one parameter out of 10 was selected as insignificant, as it had no direct, nor indirect influence on the final decision.

Choice of such models is based on the type of data and relations in the final data sample. Variables had nonlinear relationship and the model should have presented the probability of the certain outcome. Probit model should have demonstrated the influence of every parameter on the possibility of the final investment decision. Unfortunately, all the variables in the model had factor values and the model was not precise enough. This is the reason why the linear regression model were used in the research. Surprisingly, it had a 80% determination coefficient and showed the relations of variables and their influence on the final decision. Overall, the chosen methodology and model are adequate and correspond with the purpose of this research and previous studies.

The presented research is considered to partially close the academic/research gap since all the previous studies only examined the theory of evaluation parameters and checked their existence. In terms of practical importance, the paper gives important insights on the significance of every parameter, their correlation with one another and their nature. The practical importance could be for both parties of the fundraising process: Investors, mainly Venture Capital Funds and start - ups. Both parties can implement findings of this paper in their operations and strategies. VC Funds can improve their scoring and valuation frameworks. Start - ups, on the other hand, can improve or rework their fundraising strategies and focus on parameters that VC Funds consider important.

To further develop this research, first, a different data sample could be used. That will help make the model more accountable for the forecasting and prediction and will make it more precise. Usage of companies from the different fundraising stage will make the model more universal. Although, it is important to consider the differences between young and more mature companies. Secondly, created scoring system could be enriched with qualitative data instead of factor values. That will improve the probit model and improve general fitness of the model.

📕 Список литературы

🖼 Скриншоты