Тема: ACCRUAL-BASED AND REAL EARNINGS MANAGEMENT AT RUSSIAN COMPANIES: RELATIONSHIP WITH CORPORATE FINANCIAL PERFORMANCE

Закажите новую по вашим требованиям

Представленный материал является образцом учебного исследования, примером структуры и содержания учебного исследования по заявленной теме. Размещён исключительно в информационных и ознакомительных целях.

Workspay.ru оказывает информационные услуги по сбору, обработке и структурированию материалов в соответствии с требованиями заказчика.

Размещение материала не означает публикацию произведения впервые и не предполагает передачу исключительных авторских прав третьим лицам.

Материал не предназначен для дословной сдачи в образовательные организации и требует самостоятельной переработки с соблюдением законодательства Российской Федерации об авторском праве и принципов академической добросовестности.

Авторские права на исходные материалы принадлежат их законным правообладателям. В случае возникновения вопросов, связанных с размещённым материалом, просим направить обращение через форму обратной связи.

📋 Содержание

INTRODUCTION 10

CHAPTER 1. THEORETICAL REVIEW OF EARNINGS MANAGEMENT 15

1.1. Definition of Earnings Management 15

1.2. Motives for Earnings Management 16

1.3. Strategies of Earnings Management 19

1.4. Methods and techniques of Earnings Management 20

1.4.1. Accrual-based earnings management techniques 20

1.4.2. Real earnings management techniques 23

1.5. Real world cases of Earnings Management application 25

1.6. Restraints of Earnings Management 27

1.7. Choice of an Earnings Management strategy and factors behind the choice 28

1.8. Timing of Real and Accrual-based earnings management 32

1.9. Influence of Earnings Management on company performance 33

1.10. Summary and Hypotheses 35

CHAPTER 2. RESEARCH METHODOLOGY AND RESULTS 38

2.1. Research Methodology 38

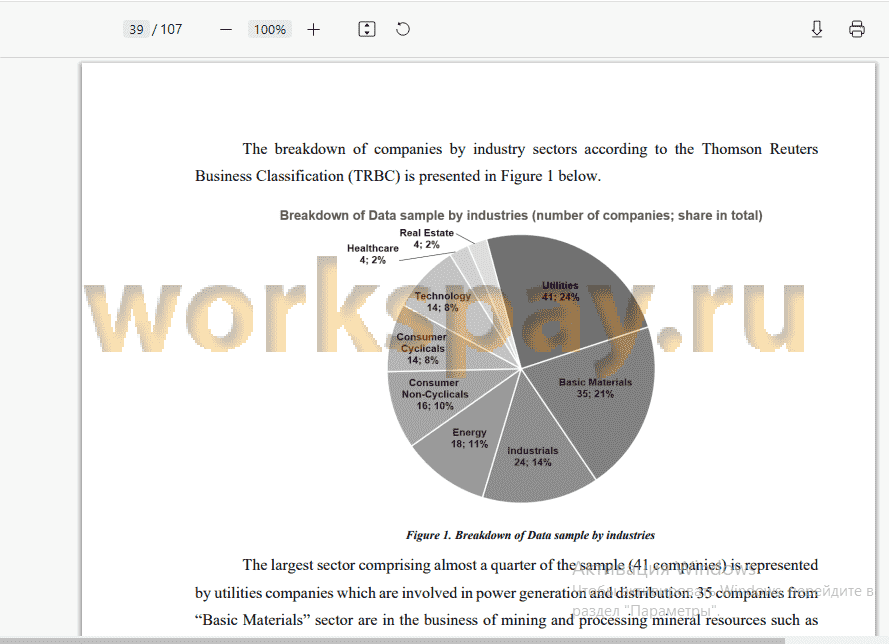

2.1.1. Data sample 38

2.1.2. Description of models and variables 40

Estimation of Earnings management proxies 40

H.1. Earnings benchmarks and earnings management 47

H.2. Factors affecting the choice of an earnings management strategy 49

H.3. Timing of Real and Accrual-based earnings management 56

H.4. Earnings management and corporate performance 58

2.2. Research results 64

2.2.1. Descriptive statistics 64

2.2.2. Empirical results 66

H.1. Earnings benchmarks and earnings management 66

H.2. Factors affecting the choice of an earnings management strategy 69

H.3. Timing of Real and Accrual-based earnings management 74

H.4. Earnings management and corporate performance 77

2.4. Discussion of results and managerial implications 84

2.5. Limitations of the study and potential for further research 87

CONCLUSION 89

REFERENCES 92

APPENDIXES 97

Appendix 1. List of Companies 97

Appendix 2.1. Correlation matrix: variables used in models to test Hypotheses 1.1. - 1.2. ...102

Appendix 2.2. Correlation matrix: variables used in models to test Hypotheses 2.1-2.6, 3 ...103

Appendix 2.3. Correlation matrix: variables used in models to test Hypothesis 4 104

Appendix 3. Panel data models selection 106

Appendix 4. Variance Inflation Factors 107

📖 Введение

Being under heavy pressure to report constantly growing earnings, managers are tempted to “decorate” financial statements and to report figures that might show a skewed picture of the company performance. It gives rise to a phenomenon of Earnings Management, an object of this study. It would be fair to note that earnings are not always managed upwards, and at times, they might be pulled down, for example, in order to create “cookie jar” reserves or for tax purposes. There exist the two earnings management strategies: accrual-based earnings management and real earnings management. The main difference between them is the influence on company operations and cash flows. Accrual-based earnings management does not affect the operational activities and is of purely accounting nature, while real earnings management presumes the interference with normal business processes and transactions. There are multiple techniques for either strategy that will be covered in details in the theoretical part of this thesis.

It is important to emphasize that earnings management is different from a fraud. Earnings management is a legal practice within the boundaries of accounting standards which provide a certain level of leeway for the accountants. The main idea behind contemporary accounting frameworks such as IFRS is the economic substance over form. In order to meet this goal, managers are required to apply their expert judgement. Since it is impossible to create hard standards suitable for all companies, standards have loopholes that might be exploited. However, the border between fraud and earnings management is very thin, and as was revealed by Perols & Lougee (2011), companies that manage earnings are more likely to commit a fraud. That is what makes earnings management a widely discussed topic attracting ever growing attention of academics and practitioners, especially after a series of large corporate scandals in beginning of 2000s.

Globally, research on earnings management started in the 1980s, and to date there have been produced a number of publications on the topic. Researches try to find the ‘best’ model to detect earnings management, study the motives for earnings management, and try determine the setting in which earnings management is more likely to occur. Another body of research focuses on strategies and instruments of earnings management and factors that influence the choice of these instruments. Though the most controversial part of research is around the influence of earnings management on subsequent company performance and value.

Unfortunately, for emerging markets and particularly for Russia, the topic remains relatively unexplored as compared to the developed countries. There are the two main reasons for that. Firstly, local researches mostly focus on fraud and disregard earnings management as such, since it is not a criminal act and implies no legal consequences. Secondly, investigation of earnings management requires large corporate datasets which started to pile up not so long ago, especially if IFRS data is considered.

One of the aspects of earnings management in Russia that has not yet gained any coverage in academic literature is the association between earnings management and company performance. Moreover, foreign researchers have not yet come to a consensus on how earnings management affects subsequent performance. One group of researchers concluded that earnings management, and particularly real earnings management, is opportunistic and leads to deterioration in subsequent company performance (Cohen & Zarowin, 2010; Legget et al., 2016; Tabassum et al., 2015). In sharp contrast to them, the other group of researchers found a positive relationship, and proposed an informational perspective in line with a signaling theory (Beyer et al., 2018; Gunny, 2010; Chen et al., 2010). As per this theory, managers, who are more informed about the true financial state of the company and company’s future prospects, use earnings management to give positive signals to the market when they believe that future results will improve. It implies that managers are well aware of side effects of an earnings management, and will apply it only when they have an understanding of future business growth and have positive news to be signaled to the market. Moreover, earnings management that aims to achieve smoother earnings might help to reduce a cost of debt and trade better terms with suppliers and customers, what in the end may positively influence on performance.

Therefore, the goal of the thesis is to investigate the influence of accrual-based and real earnings management on subsequent company performance using the sample of Russian companies.

In order to achieve the research goal and to form a better understanding on the phenomenon of earnings management, a number of research objectives were formulated. The completion of these objectives will not only help to reach the research goal, but can also produce the outcomes

that might contribute to the literature on earnings management in Russia, since a research gap on these issues exists as well....

✅ Заключение

In order to reach the research goal and to form a better understanding on the phenomenon of Earnings management, the following interim objectives were completed:

1. establishing the presence of earnings management and determination of the setting, in which companies tend to manipulate with earnings;

2. discovering the relationship between earnings management strategies (accrual-based vs. real) and defining the factors that influence on choice of either strategy;

3. identification of the timing patterns in which earnings management strategies are used;

4. understanding how either of earnings management strategies affects subsequent corporate performance

On the way to complete these objectives, the first step was to develop a theoretical framework in order to form a solid understating on the topic and to get acquainted with the current state-of-art in the global research. At first, the concept of earnings management was defined, and the main motives for earnings management were determined. Next, the two earnings management strategies (accrual-based and real earnings management) were discussed with detailed description of techniques for both strategies with follow-up real world examples of their application. Then, discussion proceeded to the restraints for earnings management and factors behind the choice of an earnings management strategy. Theoretical part was finalized with the discussion of potential influence of earnings management on corporate performance. Development of theoretical framework helped to identify a research gap and formulate the research questions and hypotheses.

The second part of the work is devoted to research design and presentation of results. The research was based on IFRS data. The panel dataset comprised data on 170 Russian non-financial public companies collected over a decade between 2011 and 2020. Investigation of earnings management in Russia based on IFRS reports complements existing publications that are in their majority based on figures prepared under Russian Accounting Standards.

The first finding is that companies, whose earnings are slightly above zero (earnings are in range 0 - 1% of lagged total assets) or slightly higher than previous year earnings (year-on- year change in earnings is in range 0 - 1% of lagged total assets), show signs of upwards earnings management. Moreover, it was revealed that a need to meet zero earnings benchmark induces real earnings management behavior, while a last year earnings benchmark is associated with accrualbased earnings management. This research was the first attempt to find an association between 89

earnings management and earnings benchmarks in Russia. The main implication of the finding is a call for a more thorough analysis of financial statements if earnings are just above the benchmarks.

Next, it was revealed that real and accrual-based earnings management have a substitutive nature, and the choice of either strategy depends on accounting flexibility, company financial health and external economic and regulatory environment. Quality and tenure of external auditor, and institutional ownership showed no significant association with either of earnings management strategies, contrary to the expectations.

Then, it was revealed that both strategies are used in a sequence, with real earnings management used first until the year-end, and after the fiscal year end, managers might apply accrual-based earnings management to fine tune the result. But, the relative use of either strategies is still influenced by the factors described above and the magnitude of accrual-based earnings management additionally depends on the outcome of real earnings management.

These findings might pose interest for researches as well as for practitioners. Researches might pay attention to the substitutive nature of earnings management that advocates for the need to study both strategies in aggregate. Policy makers might note that regulations cannot completely eliminate earnings management as such. Hence, it might be worthwhile to decide whichever type is less harmful for investors and other stakeholders in order to frame legislation in a way as to maintain the balance among all stakeholders. Investors, board members and auditors might consider these factors as an extra hint that points at the area that needs a closer look in course of their analysis.

Finally, it was concluded that real earnings management negatively influences on subsequent operating performance, measured with ROA adjusted for industry median. However, no conclusion could be made regarding the accrual-earnings management and its relative influence as compared to real earnings management.

Industry analysis revealed similar patterns. Companies from “Energy” and “Basic materials” sectors which practiced real earnings management had a weaker industry-adjusted next year profitability as compared to profitability of the companies less involved in real earnings management. These two sectors taken together represent a third of the data sample. Accrual-based earnings management also showed negative influence on profitability but only for the “Consumer Non-Cyclicals” sector. However, since this sector makes up only 10% of the whole sample and since relationship between AEM and performance for other sectors is not significant, overall, the association between the accrual-earnings management and performance is not significant as well.....

📕 Список литературы

🖼 Скриншоты